victims for over 25 years.

What is Collision Insurance?

I spend a lot of time in my articles talking about why you need Underinsured Motorist Coverage (UIM), but I also get asked about the many other types of auto and motorcycle insurance policies that you should have. And no wonder: insurance is a very confusing industry. Not only does each state have different laws guiding what kind of insurance you must carry, as well as the minimums required, but each insurance company offers these items differently.

I often get asked the following questions:

- What is collision insurance?

- What is comprehensive insurance?

- What is liability insurance?

- What is the minimum auto insurance required in Colorado?

- Why do I need underinsured motorist coverage if I have collision insurance?

Let’s get into the weeds so that you can fully understand the different types of auto and motorcycle insurance.

In this article, I’m going to break down each of those questions to help you better understand what you need to have legally in the state of Colorado and what you should have to protect yourself properly. (As I’ve said in the past, there is no magical pot of money when you get hurt in an accident. If the other driver isn’t insured properly, you need to have enough insurance to cover your own expenses.)

Questions to Ask Yourself When Buying Auto or Motorcycle Insurance

While there are legal requirements guiding what kinds and amounts of auto and motorcycle insurance you purchase, you need to also think about your personal needs beyond the bare minimum. Here are a few suggestions for you to consider from the National Association of Insurance Commissioners.

While there are legal requirements guiding what kinds and amounts of auto and motorcycle insurance you purchase, you need to also think about your personal needs beyond the bare minimum. Here are a few suggestions for you to consider from the National Association of Insurance Commissioners.

Your policy should:

- Provide at least the minimum coverage that your state’s laws require. (I’ve included Colorado’s mandates later in this article.)

- Provide enough liability coverage to pay someone else for their property damage, medical care and other costs that you may cause.

- Provide you with enough coverage to pay for your own property damage (collision insurance), medical care (medical payments coverage) and other costs (UIM) if you are in an accident.

- Provide coverage for all members of your household, including students away at school or other adults who live with you.

Does your current policy adequately address all of these areas? If you’re not sure, call your insurance agent for a policy review.

Now, let’s get into the weeds so that you can fully understand the different types of auto and motorcycle insurance. (You might keep this article handy and use it as a checklist when you’re talking to your insurance agent!)

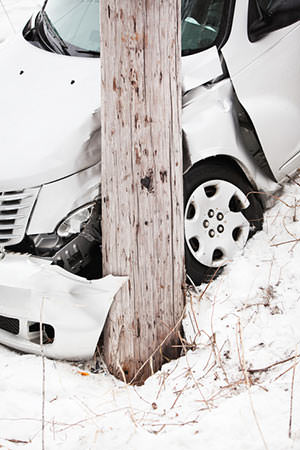

What is Collision Insurance?

Collision car insurance protects your car when it is involved in a crash with another vehicle or a stationary object. Most car crashes and auto accidents fall under this kind of insurance policy. The types of damages include crashing into another vehicle, another vehicle colliding with yours, or ramming into a streetlight, pole, or some other stationary object. It’ll cover the cost of repairs or replacements to your own car (liability coverage takes care of damages to other people’s property). However, this coverage will not pay for any medical bills you incur.

Collision car insurance protects your car when it is involved in a crash with another vehicle or a stationary object. Most car crashes and auto accidents fall under this kind of insurance policy. The types of damages include crashing into another vehicle, another vehicle colliding with yours, or ramming into a streetlight, pole, or some other stationary object. It’ll cover the cost of repairs or replacements to your own car (liability coverage takes care of damages to other people’s property). However, this coverage will not pay for any medical bills you incur.

In Colorado, collision coverage is not required by law, though your bank may require it if you have an auto loan.

What is Comprehensive Insurance?

Comprehensive car insurance doesn’t give you complete coverage, contrary to what its name might indicate. Comprehensive car insurance just covers damages to your vehicle not caused by a collision, and car owners can be surprised by how much this can encompass. Comprehensive coverage generally falls under “acts of God or nature”, that are typically out of your control when driving – a spooked deer, a heavy hailstorm, a carjacking, etc.

In Colorado, comprehensive auto insurance is optional coverage, though your bank may require it if you have an auto loan.

In Colorado, the hit-and-run statistics look like an epidemic.

What is Liability Insurance?

Liability car insurance covers damages to another person resulting from an accident that you cause. If you cause an accident, liability coverage will help you pay for damage to another person’s property or for costs associated with their injuries. (Your liability coverage doesn’t pay for any of YOUR expenses related to any accident ever. It pays for damage and injuries that you cause.)

There are two types of liability coverage:

- Bodily injury liability (BI) covers you if you cause an accident in which someone else is hurt or killed. Colorado requires limits of $25,000 per person for bodily injury, $50,000 per accident for bodily injury—commonly expressed as “25/50” on your insurance card. However, many financial experts recommend carrying at least $100,000 per person and $300,000 per occurrence – commonly expressed as “100/300.”

- Property damage liability (PD) covers you when you damage someone else’s property. Usually it’s someone else’s car, but it could apply to buildings, utility poles, garage doors, and other physical property. Colorado requires a limit of $15,000 per occurrence.

What is Medical Payments Coverage?

Medical payments coverage (Med Pay, or MPC) covers first responders, emergency room bills, co-pays, deductibles, doctor visits, chiropractors, massage therapy, physical therapy… in essence, it may cover a lot of things that your health insurance doesn’t. And if you die, your family can use it to pay off the bills that may have stacked up in the medical efforts that failed to save your life.

Medical payments coverage (Med Pay, or MPC) covers first responders, emergency room bills, co-pays, deductibles, doctor visits, chiropractors, massage therapy, physical therapy… in essence, it may cover a lot of things that your health insurance doesn’t. And if you die, your family can use it to pay off the bills that may have stacked up in the medical efforts that failed to save your life.

Colorado insurers are required to offer you $5,000 in MedPay coverage. You must opt out or the coverage and premium will automatically be added—whether you’re buying a new policy or renewing one.

Read more about the benefits of Med Pay.

If I Buy all of the Insurance Required by Colorado Law, Why Do I Need Underinsured Motorist Coverage?

You should always (always, always) have Underinsured Motorist Coverage (UIM) on every car that you own. UIM kicks in when you’re the victim in a car accident and the other driver doesn’t have enough coverage to pay for your bills. As I’ve said, in Colorado where the hit-and-run statistics look like an epidemic, you need UIM more than ever. I recommend a minimum of $250,000 of UIM because it covers medical deductibles, medical bills, medical co-pays, pain and suffering, lost wages and other economic losses.

This is typically the “pot” from which those huge settlements that you see on TV come from. If you don’t have UIM, and the other driver only has $25,000 (the minimum required by the law), you will only get $25,000, which probably won’t even come close to covering your expenses.

In Colorado, insurers are required to offer UM/UIM in the same amount as the bodily injury liability limits you select. UM/UIM can be waived only if it’s rejected in writing. Don’t waive it; buy as much as you can afford!

Handy Chart Showing Average Insurance Premiums in Colorado

I know from my own personal shopping experience that selecting an insurance carrier can be frustrating and confusing. I’m happy to chat with you about the coverage you currently carry and what you might want to add.

Additionally, the state of Colorado hosts a handy, interactive tool that helps you to compare your auto insurance costs to averages across the state. While it doesn’t tell you exactly what you should be paying, it can help you to understand if your premiums are high or low compared to others like you. This can be a nice bit of information when you’re shopping around.

And, as usual, please call me with any questions – (303) 388-5304!

Related articles:

What Should You Do if You or a Loved One Has Been Injured in a Motorcycle Accident – Don’t get victimized by illegal billing practices.

Worst Car Insurance Companies – They should be on your side but our years of dealing with insurance company proves they are out to pay you as little as possible, even if the accident wasn’t your fault.